Many taxpayers assume that once the IRS assesses penalties, those amounts are fixed and unavoidable. Others believe that penalty relief is only available in rare or extreme situations. In reality, federal tax law and IRS administrative procedures recognize that taxpayers may fail to meet their obligations due to circumstances beyond their control. When this occurs, the IRS may grant relief through Penalty Abatement for Reasonable Cause. This form of relief allows eligible taxpayers to reduce or eliminate penalties if they can demonstrate that they acted responsibly but were prevented from complying due to legitimate external factors. However, reasonable cause relief is not automatic. It requires careful documentation, a clear explanation of events, and alignment with IRS standards. For individuals and businesses, properly establishing reasonable cause is often a critical step in reducing IRS liabilities and resolving tax disputes effectively.

📘 Reference: Penalty Abatement for Reasonable Cause

💡 Featured Snippet: What is penalty abatement for reasonable cause? Penalty abatement for reasonable cause is an IRS relief program that allows taxpayers to have penalties reduced or removed if they can show their failure to comply was due to circumstances beyond their control and not willful neglect.

The Legal Authority Behind Reasonable Cause Relief

Penalty abatement for reasonable cause is grounded in Internal Revenue Code §6651 and related provisions, which authorize penalties for noncompliance but also allow for their removal when reasonable cause is established. The IRS provides detailed guidance through administrative rules, including the Internal Revenue Manual, which outlines how reasonable cause is evaluated. The key legal standard is whether the taxpayer exercised ordinary business care and prudence but was still unable to comply with tax obligations. The purpose of this relief is to ensure fairness in the tax system, recognize legitimate hardships, and encourage voluntary compliance. Because these determinations are highly fact-specific, reasonable cause cases are often carefully analyzed by a Washington, DC tax litigation attorney.

📘 Reference:

Why Reasonable Cause Penalty Abatement Matters?

IRS penalties can accumulate quickly and significantly increase the total tax liability. For taxpayers who qualify, reasonable cause relief can eliminate or reduce penalties, lower overall tax debt, and prevent escalation of IRS enforcement actions. Unlike automatic programs such as First-Time Penalty Abatement, reasonable cause relief requires a detailed explanation and supporting evidence. For taxpayers, this type of relief is often essential in complex or high-value cases.

Eligibility Requirements for Reasonable Cause

To qualify for penalty abatement, taxpayers must demonstrate:

1️⃣ Reasonable Cause

The taxpayer must show that they exercised ordinary care and prudence but were unable to comply due to circumstances beyond their control.

2️⃣ Supporting Evidence

The taxpayer must provide documentation substantiating the claimed circumstances.

3️⃣ Compliance History

While not strictly required, a strong history of compliance can improve the likelihood of approval.

For taxpayers working with a Washington, DC tax attorney, presenting a well-documented and credible narrative is often the most important factor in securing relief.

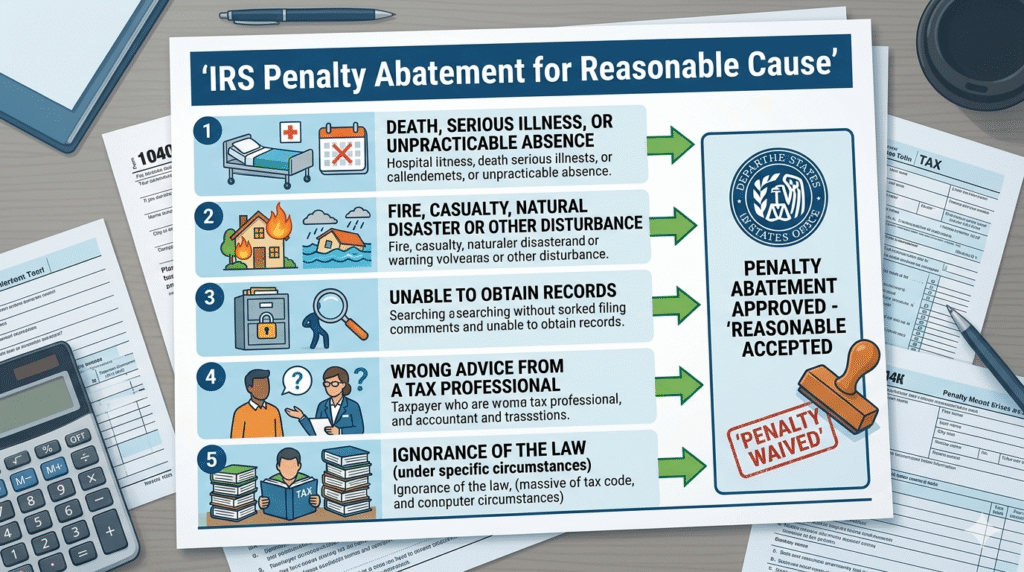

Common Situations That Qualify as Reasonable Cause

The IRS recognizes several situations that may support reasonable cause claims, including:

- Natural Disasters: Events such as hurricanes, floods, or other disasters that disrupt a taxpayer’s ability to file or pay.

- Serious Illness or Death: Medical emergencies or the death of the taxpayer or an immediate family member that interferes with compliance.

- Inability to Obtain Records: Situations where essential records are unavailable due to circumstances outside the taxpayer’s control.

- Reliance on Professional Advice: Reasonable reliance on incorrect advice from a qualified tax professional or, in some cases, the IRS.

Each of these scenarios must be supported by credible documentation and a clear explanation.

📘 Reference: IRM 20.1.1.3 – Criteria for Relief From Penalties

Common Mistakes Taxpayers Make

Taxpayers often weaken their requests by providing vague or incomplete explanations, failing to include supporting documentation, confusing reasonable cause with inability to pay, missing deadlines to request relief, and assuming relief is automatic. These errors can result in denial even when legitimate circumstances exist.

What Happens After a Request Is Submitted?

Once submitted, the IRS will review the taxpayer’s explanation, evaluate supporting documentation, consider compliance history, and issue a determination

✔️ If Approved

If approved, the penalties are reduced or removed, and related interest may also be adjusted.

❌ If Denied

If denied, the taxpayer may pursue administrative appeal, and additional legal strategies may be considered.

When to Seek Legal Guidance?

Taxpayers should consider consulting a Washington, DC tax attorney when significant penalties have been assessed, complex circumstances are involved, documentation is extensive or unclear, the IRS enforcement actions are ongoing, and previous requests have been denied. Professional guidance can improve the quality of the submission and increase the likelihood of success.

📘 Reference: IRS Form 2848, Power of Attorney

Need help with a similar issue? Contact our firm today for a consultation.

Penalty Abatement for Reasonable Cause provides an important opportunity for taxpayers to eliminate IRS penalties when circumstances beyond their control prevent compliance. While the IRS imposes penalties to encourage timely filing and payment, the law recognizes that fairness requires exceptions in appropriate cases. Successfully obtaining relief depends on presenting a clear, well-supported explanation that meets IRS standards. Taxpayers facing penalties should evaluate their eligibility early and take action to maximize available relief.

Contact Pelham PLLC, a Washington, DC tax attorney firm, for confidential assistance with IRS penalty abatement and tax dispute resolution.

FAQs

What is reasonable cause penalty abatement?

It is IRS relief that removes penalties when a taxpayer could not comply due to circumstances beyond their control.

Do I need proof for reasonable cause?

Yes, supporting documentation is essential to demonstrate eligibility.

What situations qualify?

Common examples include illness, natural disasters, or inability to obtain records.

Is financial hardship enough?

Not by itself – there must be a qualifying reason preventing compliance.

Can penalties be fully removed?

Yes, if the IRS accepts the reasonable cause explanation.

Do I need a Washington, DC tax attorney?

While not required, legal guidance can strengthen your case and improve outcomes.

{kind=link}