Most IRS collection cases begin with notices – letters requesting payment or warning of enforcement. When a case escalates to an IRS Revenue Office, the situation has moved beyond routine processing into active, field-level enforcement. IRS Revenue Officer matters present complex procedural and financial challenges for both individuals and businesses. These matters often implicate substantial liabilities and require precise knowledge of tax statutes and IRS procedures. Once a Revenue Officer takes over the case, it signals that the IRS is preparing to take direct action to collect the tax debt, including levies, liens, or asset seizure. At this stage, how you respond matters. Missteps can accelerate enforcement. The right strategy, applied quickly, can often stabilize the situation and prevent escalation.

📘 Reference: IRS Collection Process

Who Is an IRS Revenue Officer?

An IRS Revenue Officer is a field-based collection agent responsible for resolving serious or complex tax cases. Unlike auditors, they focus on collecting unpaid taxes via – among other things – financial investigation, asset analysis, and face-to-face interviews. Revenue Officers have enforcement powers, including the authority to file liens, issue levies, and garnish wages if the tax debt is not addressed. They, in addition to collection, help set up installment agreements, recommend Offers in Compromise, or deem accounts “currently not collectible” due to hardship. Revenue Officers are assigned to cases that require direct attention, typically involving larger balances or compliance issues. While Revenue Agents handle examinations(audits/checking accuracy), Revenue Officers handle collections (debt repayment).

Why Was a Revenue Officer Assigned to Your Case?

The IRS does not assign Revenue Officers to every taxpayer. Assignment usually indicates that the case meets certain criteria. Common reasons include significant unpaid tax balances, repeated failure to respond to IRS notices, defaulted installment agreements, business tax liabilities (especially payroll taxes), and indication of collection risks.

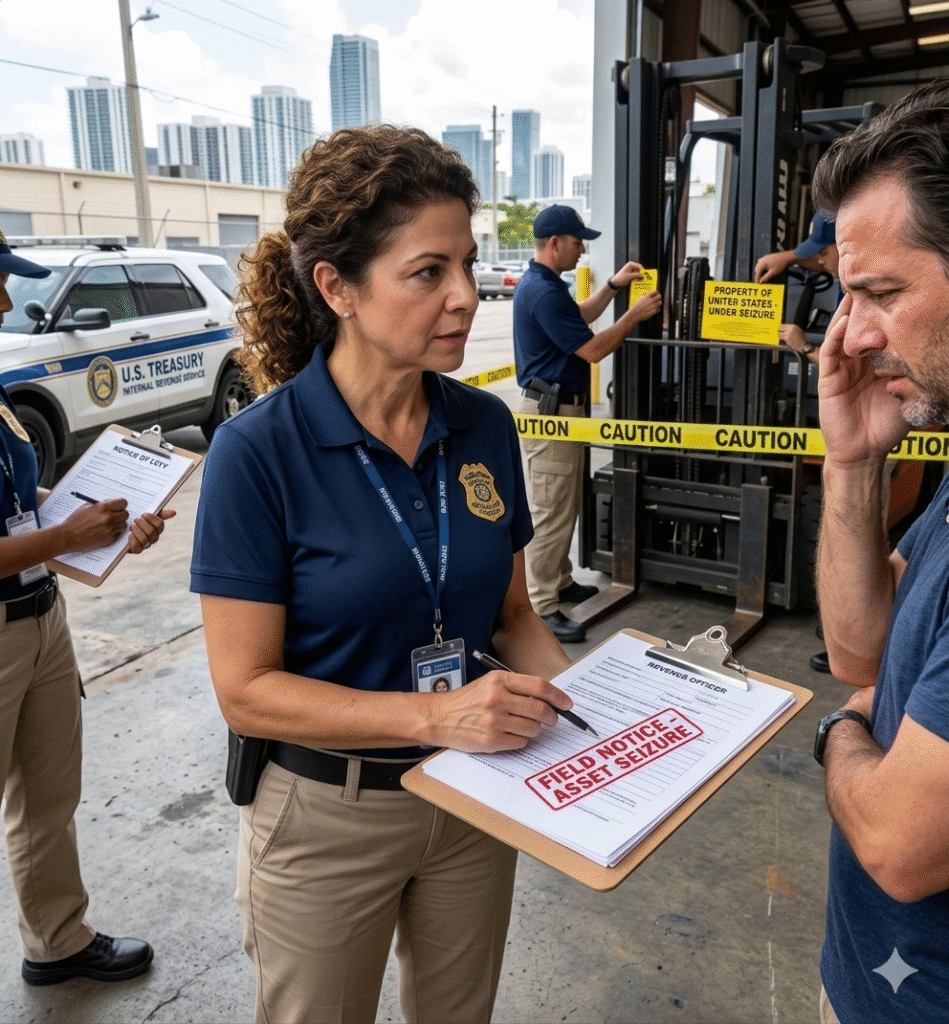

How Do IRS Revenue Officers Conduct Field Collection Actions?

Once a Revenue Officer is assigned, the case becomes more direct and more urgent. The case has moved beyond the “Automated Collection System” (letters and computer-generated notices) and into active, field-based collection. Generally, a field-based collection commences with an initial contact by the Revenue Officer requesting a meeting (in person or telephone). The purpose is to notify the taxpayer of the outstanding tax liability (often significant amounts) and demand a resolution. The Revenue Officer will request a Collection Information Statement (Form 433-A for individuals or 433-B for businesses), along with supporting documentation. The officer uses this detailed disclosure to evaluate the taxpayer’s ability to pay, determine the appropriate collection method, or set up a repayment plan. Failure to respond promptly can lead to immediate enforcement actions. Taxpayers who provide organized supporting records and have legal representation are better positioned to manage these interactions.

📘 Reference:

Why Revenue Officer Cases Are High Risk?

Unlike automated IRS collections, cases assigned to a Revenue Officer are high-risk because they are driven by human discretion rather than algorithms. In these field-level investigations, the Revenue Officer moves beyond the balance sheet to evaluate your compliance history, financial behavior, responsiveness, and “willingness to resolve” the debt. Because a Revenue Officer has the authority to issue summonses to third parties and conduct in-person interviews, an unmanaged case can lead to aggressive asset seizures.

Potential Strategic IRS Negotiation Framework of a Tax Attorney

Experienced practitioners do not use a one-size-fits-all approach; instead, they calibrate their negotiation posture based on the specific Revenue Officer assigned and the unique financial “story” of the taxpayer. A tax attorney in Washington DC, utilizes a specialized negotiation framework designed to insulate clients from IRS enforcement while aggressively pursuing debt resolution. By leveraging statutory precedents and the Internal Revenue Manual (IRM), counsel shifts the power dynamic away from the Revenue Officer and toward a structured settlement. This approach centers on three critical tactical pillars:

1️⃣ Leveraging “Hazards of Litigation”

Rather than arguing purely on financial hardship, skilled attorneys identify “litigation hazards” – legal or factual weaknesses in the IRS’s position. By demonstrating that the government faces a credible risk of losing if the case proceeds to the US Tax Court, attorneys create the leverage necessary to settle for significantly less than the original assessment.

2️⃣ Strategic Liability Reduction

Attorneys navigate the complex administrative requirements of Offers in Compromise (OIC) and Partial Payment Installment Agreements. This involves a forensic analysis of the client’s “Reasonable Collection Potential” to ensure the IRS accepts a settlement that reflects the client’s true financial capacity rather than their total paper debt.

3️⃣ Procedural Safeguards & Appeals

If a Revenue Officer remains uncooperative, practitioners deploy Collection Due Process (CDP) rights. This moves the case out of the field office and into the hands of an Appeals Officer, whose primary mandate is to resolve disputes without a trial. This step preserves the client’s assets from seizure (levy) while a final and potentially favorable resolution is brokered.

📘 Reference:

Why Timing Defines the Outcome?

In Revenue Officer cases, timing is your most valuable form of leverage. Because Revenue Officers operate on strict administrative timelines, missing a single deadline can trigger immediate levies, wage garnishments, or asset seizures. However, engaging early allows you to freeze enforcement, preserve negotiation collection alternative options, and establish the “good faith” credibility necessary for a negotiated settlement.

📘 Reference: IRS Form 2848, Power of Attorney

Need help with a similar issue? Contact our firm today for a consultation.

An IRS Revenue Officer assignment signals that your case has entered a more serious phase of collection. It does not mean the situation is beyond control. With the right strategy and timely legal intervention, enforcement can often be prevented and a workable resolution can be achieved.

Engaging a Washington DC tax attorney materially strengthens a taxpayer’s position when contesting Revenue Officer’s actions. Experienced counsel provide tailored negotiation strategies, defend procedural rights, and pursue resolutions that minimise fiscal exposure. A thorough understanding of IRS enforcement mechanisms enables clients to make informed decisions and to protect their financial interests. For case-specific guidance, contact our team to arrange a consultation.

FAQs

What should I do if I receive a notice from an IRS Revenue Officer?

Consult a tax attorney experienced in Revenue Officer matters.

Who is an IRS Revenue Officer?

An IRS Revenue Officer is a field agent who handles serious tax collection cases and can take enforcement action.

What are the potential consequences of not cooperating with an IRS revenue officer?

Non-cooperation may prompt the IRS to intensify collection actions, including filing federal tax liens, initiating levies, garnishing wages, or seizing assets. Non-compliance can also increase penalties and interest.

Why was a Revenue Officer assigned to my case?

Usually due to large tax debt, missed payments, or unresponsive behavior to prior IRS notices.

Can a Revenue Officer come to my home or business?

Yes. Revenue Officers may conduct in-person visits to collect information or enforce compliance.

What is Form 433 and why is it important?

Form 433 is a financial disclosure form used by the IRS to evaluate your ability to pay.

Can a Revenue Officer levy my bank account?

Yes. They can initiate levies, wage garnishments, and file tax liens.

How do I stop IRS enforcement actions?

By responding quickly, providing accurate financials, and negotiating a resolution such as a payment plan or hardship status.

Should I speak directly to a Revenue Officer?

You can, but it is often best to have a tax attorney handle communications.

Can a tax attorney stop a Revenue Officer case?

An attorney can often prevent escalation and negotiate a resolution to avoid enforcement.

When should I hire a tax attorney?

Immediately after a Revenue Officer contacts you or requests financial information.

{kind=link}