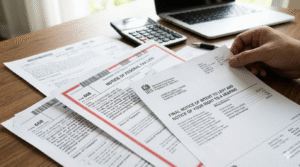

When the IRS completes an audit and determines that additional tax is owed, many taxpayers expect to receive a bill. Instead, federal tax law requires the IRS to issue a formal legal notice before it can assess and collect the tax. This document is known as a Notice of Deficiency, often referred to as the “90-day letter.” The Notice of Deficiency is one of the most important documents in the federal tax dispute process. It provides taxpayers with a limited opportunity to challenge the IRS’s determination in court before paying the disputed tax. However, that opportunity is strictly time-limited. If the taxpayer fails to act within the statutory deadline, the IRS may assess the tax and begin collection actions. At that point, the taxpayer’s ability to challenge the liability becomes significantly more restricted. For taxpayers working with a Washington, DC tax attorney, understanding how the Notice of Deficiency operates is critical to preserving legal rights.

📘Reference:

What a Notice of Deficiency Is?

A Notice of Deficiency is a formal IRS determination that a taxpayer owes additional tax for a specific year. It is issued after the IRS completes an audit or examination and concludes that adjustments are necessary. The notice includes:

- The amount of the proposed deficiency;

- The tax years involved;

- An explanation of the IRS’s adjustments; and

- Information about the taxpayer’s right to challenge the determination.

Unlike many IRS notices, the Notice of Deficiency is not a demand for immediate payment. Instead, it is a legal prerequisite to assessment that gives the taxpayer an opportunity to contest the IRS’s determination in court. For individuals and businesses represented by a Washington, DC tax attorney, this notice marks the transition from administrative audit procedures to potential litigation.

📘Reference: IRS Examination Process

The Legal Authority Behind the Notice of Deficiency

The Notice of Deficiency is governed by federal statute. Under Internal Revenue Code §6212, the IRS is authorized to issue a statutory notice when it determines that a taxpayer owes additional tax. Once the notice is issued, Internal Revenue Code §6213 restricts the IRS from assessing the tax for a specified period of time. This statutory framework provides an important protection for taxpayers. It ensures that taxpayers have the opportunity to challenge the IRS’s determination in court before the government can assess and collect the disputed tax. These provisions form the foundation of prepayment judicial review, a central feature of federal tax litigation.

📘Reference: IRC §6213 – Restrictions applicable to deficiencies; petition to Tax Court

Why the Notice of Deficiency Matters?

The Notice of Deficiency is the taxpayer’s last opportunity to challenge the IRS before assessment. It provides access to the United States Tax Court, where the taxpayer can dispute the IRS’s determination without first paying the tax. This prepayment forum is a critical advantage. If the taxpayer does not file a Tax Court petition within the required time, the IRS may assess the tax and proceed with collection actions, such as liens and levies. At that point, the taxpayer’s options are more limited and typically require payment of the tax followed by a refund claim. For taxpayers facing significant liabilities, preserving the right to Tax Court review is often essential – something routinely emphasized by experienced Washington, DC tax litigation attorneys.

📘Reference: United States Tax Court

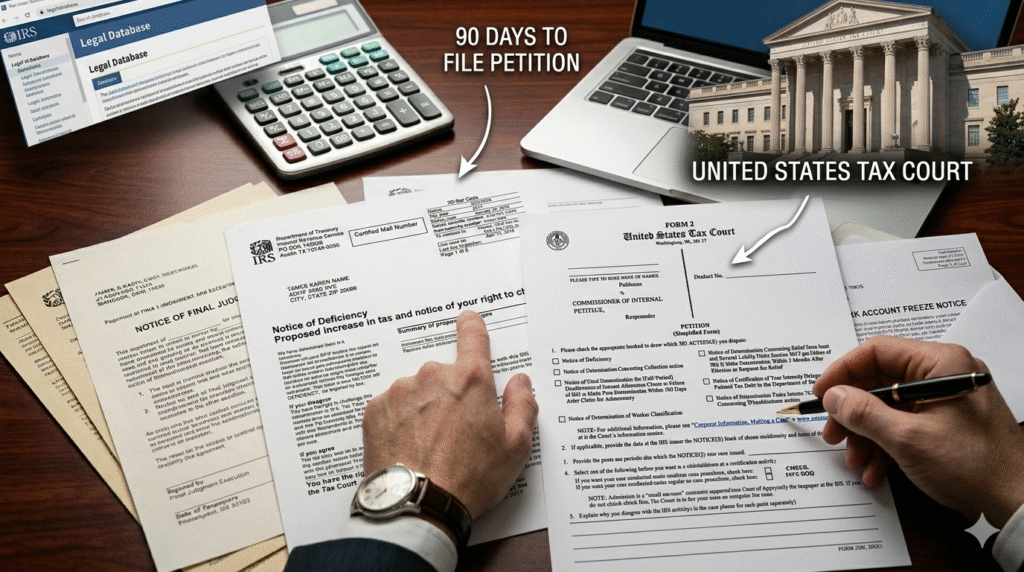

The 90-Day United States Tax Court Deadline

The most critical aspect of the Notice of Deficiency is the 90-day deadline. After the notice is mailed, the taxpayer has 90 days to file a petition with the United States Tax Court. If the notice is addressed to a taxpayer outside the United States, the deadline is extended to 150 days. This deadline is strict. The Tax Court treats it as a jurisdictional requirement. If the petition is filed even one day late, the court generally lacks authority to hear the case. The IRS is not required to extend this deadline, and courts have consistently enforced it. For this reason, taxpayers should act immediately upon receiving a Notice of Deficiency and consult a Washington, DC tax attorney if litigation is being considered.

What Happens After the Petition Is Filed?

Once a petition is filed, the case enters the Tax Court litigation process. The IRS Office of Chief Counsel represents the government, while the taxpayer may be represented by a tax attorney. The case generally proceeds through several stages:

- IRS files an answer;

- Parties exchange information;

- Settlement discussions occur; and/or

- Trial is scheduled if necessary.

Many cases are resolved through settlement before trial. However, if the case proceeds to trial, a Tax Court judge will hear the evidence and issue a decision. Tax Court litigation is a specialized process that often benefits from representation by a Washington, DC tax litigation attorney.

Common Mistakes Taxpayers Make

Taxpayers frequently lose their rights after receiving a Notice of Deficiency due to avoidable errors. Common mistakes include:

- Ignoring the notice;

- Misunderstanding the 90-day deadline;

- Attempting to negotiate without filing a petition;

- Filing the petition late; and/or

- Filing in the wrong court.

These mistakes can permanently eliminate the taxpayer’s ability to challenge the IRS in Tax Court. Once the deadline expires, the IRS may assess the tax and proceed with collection. Avoiding these errors is a key part of effective representation by a Washington, DC tax attorney.

📘Reference: IRS Notice of Deficiency FAQ

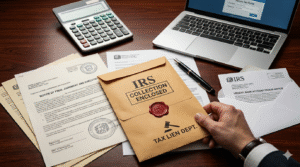

What Happens If You Miss the 90-Day Deadline?

If the taxpayer does not file a petition within the 90-day period, the IRS may assess the tax. Once the tax is assessed, the IRS may initiate collection actions, including federal tax liens, levies on bank accounts; and wage garnishment. At that point, the taxpayer generally cannot return to Tax Court.

Instead, the taxpayer may need to pay the tax in full, file a refund claim, and pursue litigation in federal court. These procedures are often more complex and costly than Tax Court litigation. For this reason, missing the 90-day deadline can significantly affect the taxpayer’s legal position.

📘Reference: IRS Collections Process

Why the Notice of Deficiency Is Frequently Misunderstood?

The Notice of Deficiency is often misunderstood because it does not resemble a traditional bill. Some taxpayers assume they can continue discussions with the IRS after receiving the notice without taking formal action. However, the 90-day deadline continues to run regardless of ongoing communications.

Other taxpayers confuse the Notice of Deficiency with other IRS notices, such as audit letters or billing statements. This confusion can lead to missed deadlines and lost rights. Working with a Washington, DC tax attorney can help ensure that the notice is properly understood and that appropriate action is taken.

📘Reference: IRS Notice Explanation

When to Seek Legal Guidance?

Taxpayers should seek legal guidance immediately after receiving a Notice of Deficiency. Legal assistance may be particularly important when:

- The amount in dispute is significant;

- The case involves complex tax issues;

- Multiple years are involved; and/or

- Litigation is likely.

An experienced Washington, DC tax attorney can evaluate the IRS determination, prepare a Tax Court petition, and represent the taxpayer throughout the litigation process. Because the deadline cannot be extended, prompt action is critical.

📘Reference: IRS Form 2848 – Power of Attorney

Need help with a similar issue? Contact our firm today for a consultation.

The IRS Notice of Deficiency is one of the most important documents in the federal tax dispute process. It provides taxpayers with a limited opportunity to challenge IRS determinations in the United States Tax Court before paying the disputed tax. However, this opportunity is strictly time-limited. Taxpayers who fail to act within the 90-day deadline may permanently lose their right to Tax Court review. Understanding how the Notice of Deficiency works – and responding promptly – can be critical to protecting your legal rights.

Contact Pelham PLLC, a Washington, DC tax attorney firm, for confidential Tax Court litigation counsel.

FAQs

What is an IRS Notice of Deficiency?

A Notice of Deficiency is a formal IRS determination that additional tax is owed and gives the taxpayer 90 days to file a petition in the United States Tax Court.

What is the IRS 90-day letter?

The IRS 90-day letter is another name for the Notice of Deficiency, which starts the deadline to file a Tax Court petition.

How long do I have to respond to a Notice of Deficiency?

Taxpayers generally have 90 days from the date the notice is mailed to file a petition in Tax Court.

What happens if I miss the 90-day deadline?

If you miss the deadline, the IRS may assess the tax and begin collection actions, and you lose the right to challenge the case in Tax Court.

Can the IRS extend the 90-day Tax Court deadline?

No. The 90-day deadline is jurisdictional and cannot be extended.

Do I have to pay the tax before going to Tax Court?

No. One of the key benefits of Tax Court is that you can challenge the IRS without paying the tax first.

What does a Washington, DC tax attorney do after a Notice of Deficiency?

A Washington, DC tax attorney can evaluate the notice, file a Tax Court petition, and represent you in litigation or settlement negotiations.

Can I still negotiate with the IRS after receiving a Notice of Deficiency?

Yes, but you must still file a Tax Court petition within 90 days to preserve your rights.

Where is the United States Tax Court located for DC taxpayers?

The United States Tax Court sits in Washington, DC and hears cases nationwide, including those involving DC taxpayers.

When should I contact a Washington, DC tax attorney about a Notice of Deficiency?

Immediately after receiving the notice, because the 90-day deadline begins running as soon as it is mailed.

{kind=link}